Fight Health Insurance Denials by Phone

80% of appealed denials get overturned. Less than 12% are ever appealed. The ladder, the peer-to-peer move, and the state-DOI vs ERISA map.

- Most initial denials are filters, not verdicts.Algorithmic rejections bank on attrition. The appeal ladder exists — and it works — but you have to start the clock.

- Peer-to-peer is the single highest-leverage move.Adds 15–20 percentage points on top of written appeals. A telephonic conversation with a medical director bypasses algorithmic rejection.

- Know your final venue before you file.Fully-insured / ACA plan → state Department of Insurance. Self-funded ERISA → federal DOL/EBSA. Wrong venue wastes the filing.

Health insurance denial is rarely a clinical verdict. It is, overwhelmingly, an administrative filter priced to capture revenue from the 99% of patients who will walk away. This guide is how to stop walking away. It covers the denial taxonomy (know what you’re fighting), the five-step appeal ladder (with timelines and success rates at each level), why the peer-to-peer call is the single highest-leverage move in the whole stack, the state-DOI-vs-ERISA split that decides your final venue, the 2024–2026 regulatory tailwinds you can cite on the call, and how to decide whether to fight it yourself or hand the telephonic parts to a service. The exact phone scripts — peer-to-peer, step-therapy exception, AI-denial challenge, ER downcoding, parity violation — live on the appeal scripts page.

The overturn gap insurers rely on

That gap — an 80% overturn rate against an 11.5% appeal rate in MA, or 83% commercial overturn against <1% commercial appeal — is not an accident. It is the financial foundation of the utilization-management model. The insurer prices the denial assuming you will not appeal. When you do, the denial very often collapses, because the algorithm that issued it could not actually defend it on clinical grounds.

Initial denials are an administrative filter, not a clinical verdict. Insurers assume 99% of patients will walk away. The whole playbook is built around not being one of them.

Know what you’re fighting — denial taxonomy

Denials have categories. Each has a different trigger, and each has a different tool that beats it. Before you call, read the denial letter for the specific reason code and match it here.

| Denial type | Typical trigger | What beats it |

|---|---|---|

| Prior authorization | Provider didn’t submit a PA, or the PA was rejected before service. | Urgent: expedited appeal (72 hours). Non-urgent: Level 1 + peer-to-peer. |

| Medical necessity | Clinical-criteria algorithm says the service isn’t justified for the diagnosis. | Peer-to-peer with NCCN / ACP / AAFP guideline citation. |

| Step therapy / tier exception | Insurer demands “fail first” on a cheaper drug before authorising the prescribed one. | Document contraindications to the preferred drug; file a step-therapy exception by phone. |

| Out-of-network / ER | Claim denied because provider was out-of-network (ER or otherwise). | No Surprises Act: emergency services must be covered at in-network cost-sharing, no PA required. |

| ER downcoding | Insurer retrospectively decides the ER visit wasn’t an emergency based on the final diagnosis. | Prudent-layperson standard — coverage is based on presenting symptoms, not the ultimate diagnosis. |

| Coding / bundling | CPT/HCPCS codes don’t match ICD-10, or procedures unbundled that should be bundled. | Clinic billing correction + resubmission; often a 5- minute phone fix. |

| DME | Wheelchair, CPAP, oxygen tank denied for not meeting qualifying thresholds. | Certificate of Medical Necessity + face-to-face evaluation notes; three-way with provider & vendor. |

| Experimental / investigational | Insurer claims the therapy lacks peer-reviewed efficacy, regardless of FDA status. | Cite FDA approval for the indication + clinical guideline; external IRO review almost always reached. |

| Mental-health parity violation | Insurer caps behavioral-health visits or imposes concurrent review not applied to medical/surgical care. | MHPAEA 2024 final rules: NQTL violation, file with DOL. |

| AI / algorithmic | Bulk rapid denial, no individual physician review. | Demand human-physician review under CA SB 1120 / AZ HB 2175 / MD HB 820. |

Sources: AMA 2022 prior-authorization survey, HHS OIG Medicaid MCO report, CMS Medicare Advantage denial data, and the 2024–2026 anti-AI-denial legislative stack.

If you are a caregiver navigating these on behalf of a dependent, the HIPAA-authorization mechanics that unlock your ability to appeal at all are covered on the caregiver phone checklist.

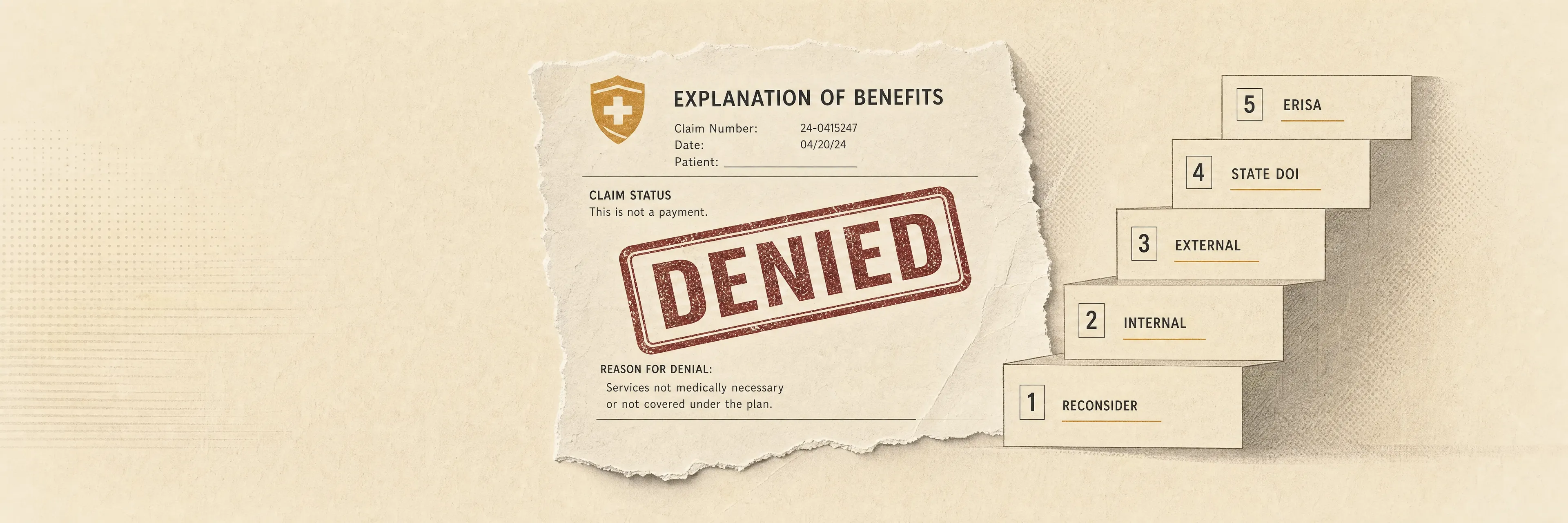

The appeal ladder — five levels, with timelines

The appeals process is a legally protected ladder. Each step is a separate filing with its own deadline and its own reviewer. Strict adherence to the filing window is non-negotiable — miss it and the claim closes.

- 1

Internal reconsideration

A written request asking the insurer to review its own decision. By law, a different medical reviewer must look at the case. Quick win if the denial was clerical (wrong diagnosis code, missing document).

- 2

Peer-to-peer physician review

A telephonic conversation between your treating physician and the insurer's medical director. The single highest-leverage move — adds 15–20 percentage points on top of a written appeal. Real-time clinical context bypasses algorithmic rejections.

- 3

Level 2 internal appeal

Required by some plans before external review. A panel of clinicians and administrators re-examines the case. Bring new evidence — updated imaging, additional guideline citations, a second-opinion note.

- 4

External IRO review

Third-party, state- or federally-contracted physician panel with no financial tie to the insurer. Free to the patient. Uses broader medical criteria than the insurer's proprietary policy. Available whenever the denial involves medical judgment.

- 5

State DOI complaint / ERISA DOL

Final administrative recourse. Fully-insured and ACA plans go to your state Department of Insurance (or the NAIC consumer portal). Self-funded ERISA plans go to the federal Department of Labor's Employee Benefits Security Administration (askebsa.dol.gov). Escalation letters force the insurer to justify the denial against state parity laws and federal statute.

For urgent, life-threatening care, all five levels have an expedited variant that compresses the decision window to 72 hours. Invoke it explicitly when filing: the insurer is legally obligated to route expedited requests separately.

Why peer-to-peer is the killer move

Written appeals succeed roughly 67% of the time on their own. Adding a peer-to-peer review pushes the overturn rate up by an additional 15–20 percentage points. It works because the treating physician can bypass the clinical-criteria algorithm that issued the denial and explain real-time context — contraindications to the insurer’s preferred alternative, failed prior conservative therapy, unusual comorbidities — directly to a human reviewer who has authority to overturn on the spot.

The routing detective work catches most caregivers off guard. Many large insurers outsource specialty denials to sub-contractors. Cigna and Humana, for example, route specialty-imaging denials (MRI, MSK, oncology) through EviCore, and post-acute Medicare Advantage denials through HealthSpring. Calling the primary insurer’s general line for an EviCore denial leads to a procedural dead end. The denial letter names the reviewing entity — always use that number, not the back of your insurance card.

Your treating physician must bring three specific pieces of evidence to the peer-to-peer call: (1) the insurer’s own Clinical Policy Bulletin / Medical Coverage Policy cited in the denial, (2) a national clinical guideline supporting the treatment (NCCN for oncology, ACP or AAFP for primary care management), and (3) a concrete timeline of conservative therapies the patient has already tried and failed, which neutralises “step-therapy” arguments before they start.

The peer-to-peer itself is physician-to-physician — your doctor runs that conversation. The part Pallie can absorb is everything that surrounds it: scheduling, holding, verifying the correct sub-contractor, following up for the written decision. Get the exact peer-to-peer script.

State DOI vs ERISA — decide your venue first

The final administrative recourse depends on how your plan is funded. Get this wrong and you file with an agency that cannot help. Check your Summary Plan Description for the phrase “self-funded” or “self-insured” — that single keyword decides the path.

State DOI

- File with your state Department of Insurance — every state has an online consumer complaint portal

- Or use the NAIC cross-state portal at naic.org

- Submit denial letters, Explanation of Benefits, medical records, physician letters

- Regulator compels the insurer to justify the denial against state parity laws

Federal DOL / EBSA

- File with the Employee Benefits Security Administration at askebsa.dol.gov or call 1-866-444-3272

- Submit plan documents, Summary Plan Description, evidence internal appeal was exhausted

- State-level protections (and state DOI) do NOT apply — ERISA pre-empts

- Final legal recourse is federal-court ERISA litigation

Regulatory tailwinds to cite on the call (2024–2026)

Four regulatory shifts give you concrete legal levers retention agents and medical directors are trained to respect. Name the rule when you call — it de-escalates quickly.

The practical move on the call: when appealing, explicitly demand written confirmation that a licensed physician — competent to evaluate your specific clinical issue — independently reviewed the case. If the denial was algorithmic and the insurer operates in a state with one of these laws, the denial is procedurally defective and should be reversed on that basis alone.

When DIY isn’t the right tool — the delegation matrix

The appeals market has split into distinct delegation tiers. Each addresses a different level of burden, and the right choice depends on whether your blocker is the writing, the phone time, or the clinical argument itself.

| Service | Cost | Speed | Scope | Best for |

|---|---|---|---|---|

| Claimable | $39.95 flat | Minutes | Generates appeal letter; mails/faxes it | Specialty-drug denials, obesity medications, imaging appeals where the written letter is the lever. |

| Counterforce Health | Free | Minutes | AI appeal letter generator, NIH-grant-funded, strict citation to clinical literature | High-cost drug / standard necessity denials when budget is zero and evidence exists. |

| Private patient advocate | $100–$500 / hour | Days | Full telephonic + administrative takeover; hospital, insurer, state DOI | Multi-layered cases: rare comorbidities, out-of-network surgical negotiations, dual-eligibility failures. |

| Enterprise voice AI (clinic-side) | B2B, ~$300+/mo | Real-time | Voice bots that absorb IVR, schedule, chase claim status for clinics | Not consumer-accessible. Benefits you indirectly when your clinic deploys it. |

| Pallie Calls | Flat per-call | Real-time | Voice concierge absorbs hold time; files Level-1 appeals by phone; schedules peer-to-peer; tracks IRO submission | When the telephonic labor is the blocker and your clinician already has the clinical argument ready. |

Non-medical bills — different playbook entirely

If the denied charge is actually a cable, mobile, insurance, or gym bill, none of this applies. Retention departments work on churn economics, not on utilization-management statute. Different script, different levers, different venue. The bill-negotiation pillar covers that playbook end-to-end. Don’t try to apply medical-appeal tactics to a cable bill — you’ll lose the window to the much simpler retention call.